May 11, 2024 • 4 min read • Private Credit

“Private credit” is a term that defines any private loan issued by a non-bank lender that is not publicly issued or traded. The form of debt financing is generally extended to companies that do not qualify for traditional bank funding and are not listed on stock exchanges. Consequently, these loans are often offered at higher interest rates to offset the risk and illiquidity associated with this type of financing.

U.S. investors have recently demonstrated an appetite for private credit investments in their portfolios, given the premium on yield versus traditional investment-grade bonds. The private credit market has doubled since just before the dawn of the COVID era. We explore why below.

After the Great Financial Crisis of 2008, regulators implemented stricter regulations on banks via the Dodd-Frank Act of 2010. The Dodd-Frank Act helped boost private lending from non-bank firms. This, in turn, forced many small-mid size indebted companies to seek alternative financing.

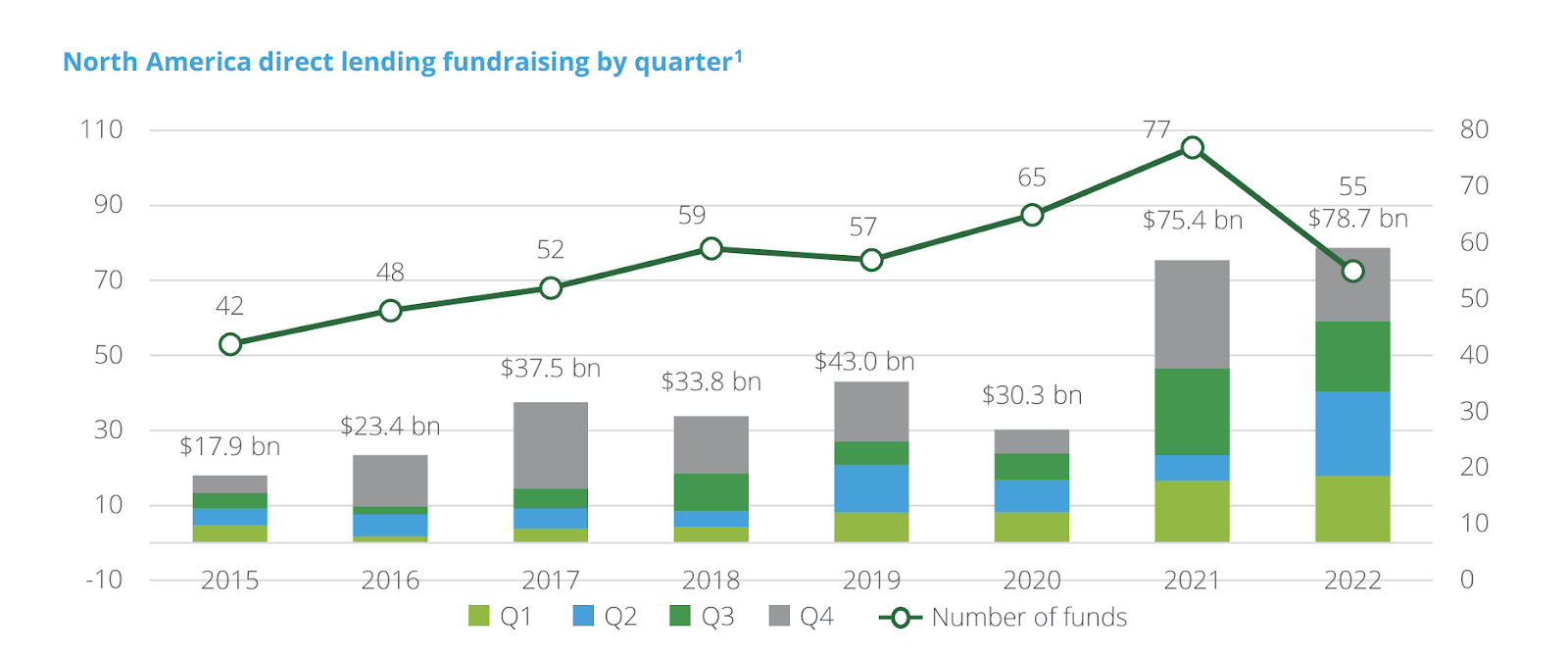

The private credit market has continually increased over the last decade. Post-Covid, substantial capital has been invested with private credit sponsors (see chart 1). A private credit sponsor is a firm that raises capital from investors to issue the capital as loans to middle-market companies.

Chart 1

Understanding Private Credit

Why has private credit transaction volume increased substantially in the last decade? A few reasons:

- Regional bank failures, like Silicon Valley Bank’s collapse in 2023, forced banks to shore up liquidity.

- Public markets are getting smaller. Companies are foregoing the IPO route and remaining private — turning to alternative sources of capital.

- Lower rates in the early 2000’s pushed investors to seek higher yield in the private debt markets.

- Mergers & acquisitions (M&A) activity post-COVID has pushed private equity sponsors to tap alternative sources in order to fund their portfolio companies.

The risk associated with a private credit loan is heavily tied to the following:

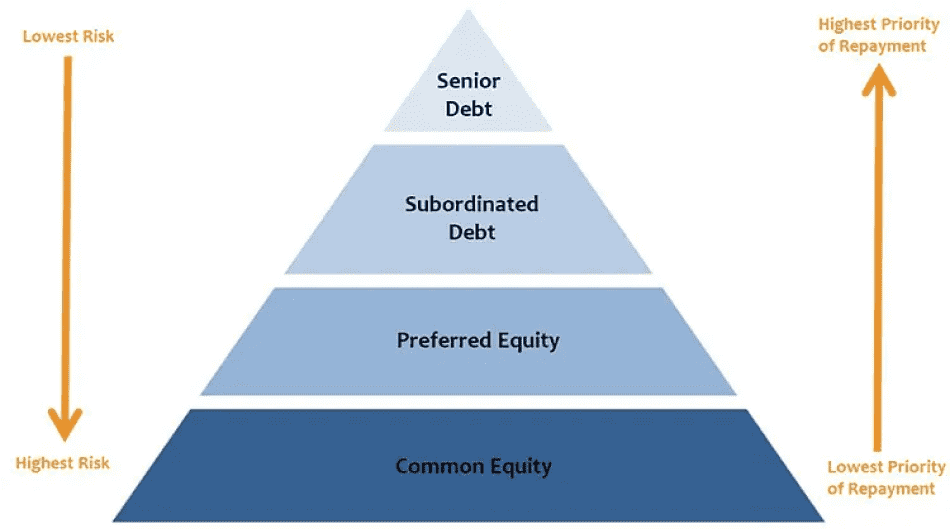

- Seniority: Based on the seniority level, investors require specific levels of returns. More risk equates to higher expected reward (see chart 2 & 3 below).

Chart 2

- Covenants (protections on debt)

- Incurrence covenant examples:

- Limitations on additional debt

- Restrictions on capital expenditures

- Restrictions on asset sales

- Maintenance covenant examples:

- Debt service coverage ratio requirements

- Minimum Current Ratio requirements

- Leverage ratio requirements

- Incurrence covenant examples:

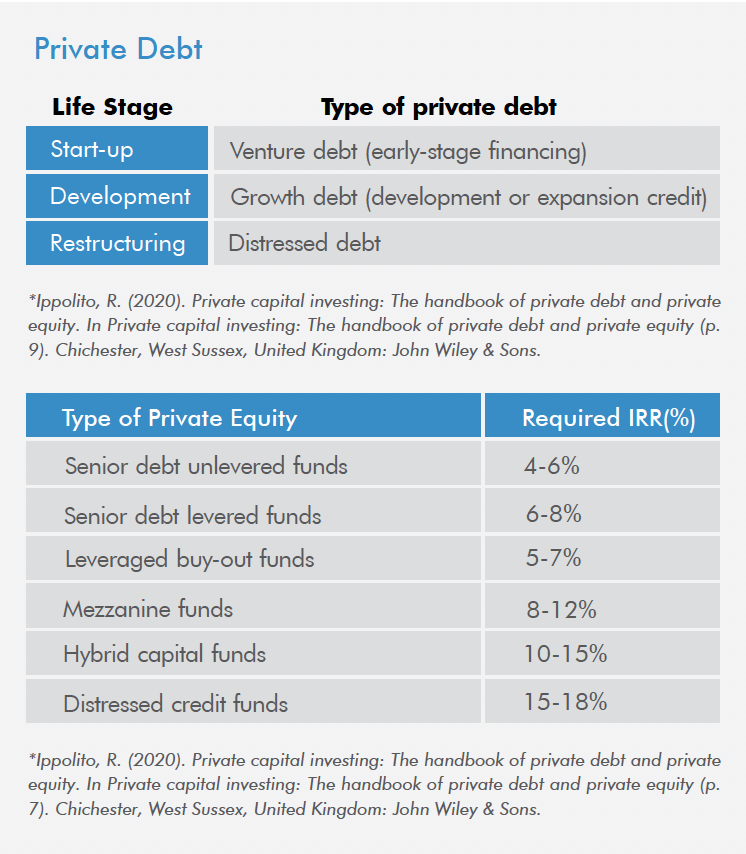

- Life stage

- Start-up: Venture debt (early-stage financing)

- Development: Growth debt (development or expansion)

- Restructuring: Distressed Debt

Chart 3

A Good Sign

Most of the allocated private debt since 2020 has been issued to ‘sponsor-backed’ portfolio companies for the purposes of M&A. ‘Sponsor-backed’ means the borrowers are backed by private equity (PE) company investments. Good PE firms are known to support their portfolio companies — often assisting in growth and management decisions. M&A activity in the last three years is led by the healthcare & life sciences, professional services, and media & telecommunications sectors.

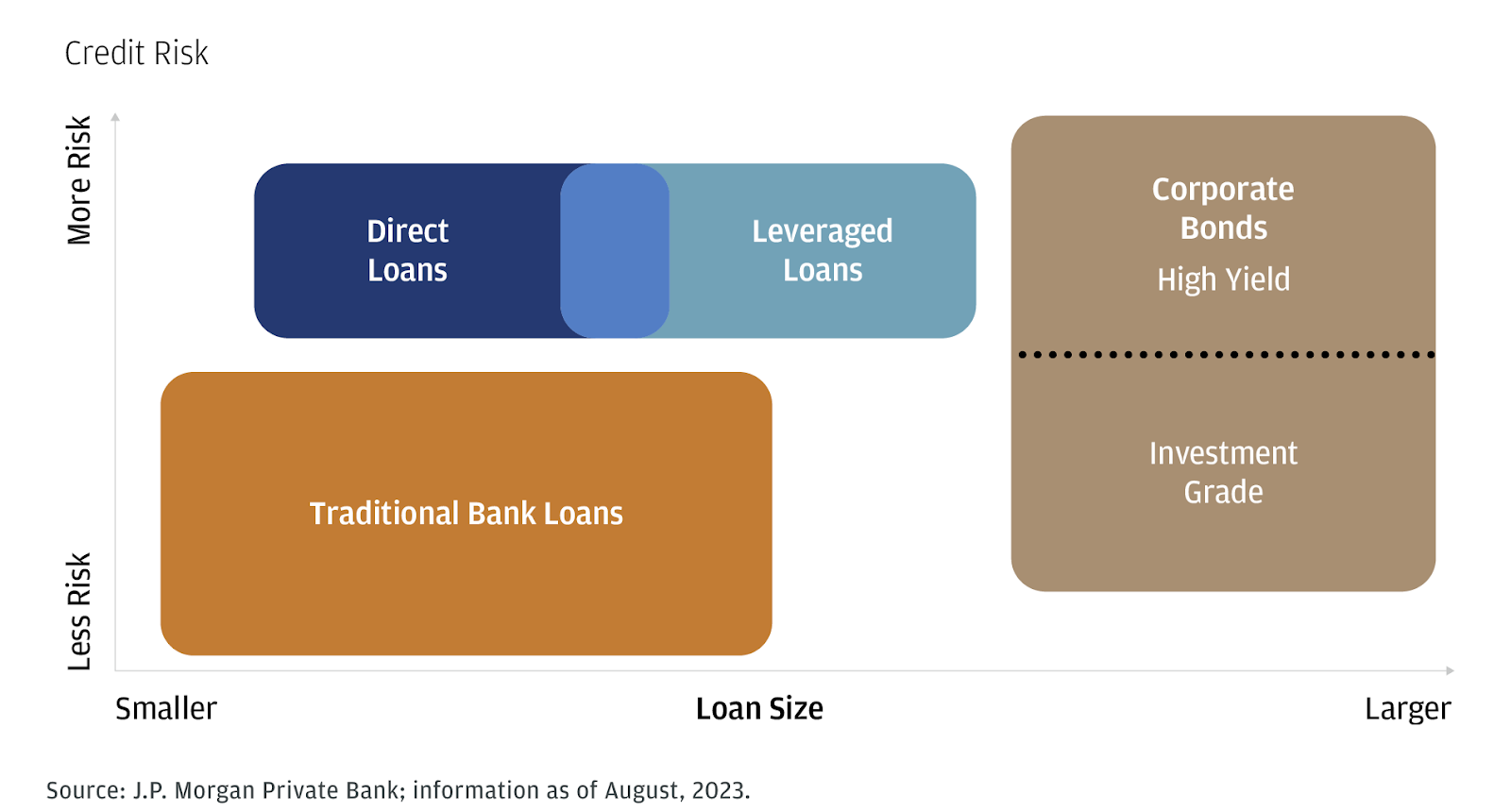

It is noteworthy that the borrowing companies are taking on debt for expansion, versus distressed situations. Moreover, direct lending by non-banks is not overhauling corporate leverage, but is ‘filling the gaps’ for companies in need of small-midsize loans (see chart 4).

Chart 4

Chart 4

Increasing corporate profits also provide comfort to private credit investors.

Chart 5

Drawbacks

Let's examine some of the drawbacks in private credit investing:

- Borrowers are typically below investment grade, meaning less-healthy balance sheets

- Lesser transparency to investors as private companies do not disclose financial statements publicly

- Companies pay higher yield to investors to compensate for the illiquidity, which may impact interest coverage ratios

- Direct loans are typically floating rate, meaning higher interest rates can pose a threat to the borrowers liquidity

The Road Ahead

Private credit lending has slowed in 2023 from its peak in 2021-2022, mainly as a result of lower M&A activity in the market. Should rates continue to move lower, the appeal of private credit may lessen as yields spreads tighten. Moreover, recent market activity shows that Wall Street banks are returning to the lending market.

Considering the pros and cons of private credit investing, this asset class is better served for investors with a higher risk tolerance. Investors should remain conscious of the illiquid nature of such investments. For those investors with ample liquidity and a higher risk tolerance, private credit investments can help generate a premium on income when compared to bonds.

Yieldwink

Yieldwink